Oil, Inflation, Wages, and the Debt Clock

Venezuela is at an inflection point that matters well beyond its borders. After years of economic collapse and political isolation, the country is simultaneously re-engaging with international financial institutions, announcing a restructuring of $159 billion in public external debt, and reopening its oil sector to foreign investment. For development practitioners, sovereign creditors, energy investors, and policymakers tracking Latin America, the decisions being made right now about sequencing, legitimacy, and fiscal discipline will determine whether Venezuela achieves a durable stabilization or locks in another cycle of partial reform and reversal. This article draws on DevTech’s macroeconomic modeling and the latest available data to assess where things stand as of mid-2026.

01 / Reducing the Free Fall, Not Yet Closing the Gap

The Trump Administration has framed its approach to Venezuela as a sequenced three-step program: stabilization, economic recovery, and democratization.1 The first step is designed to halt the free fall in output and confidence rather than deliver a full recovery. By that limited standard, results in the first half of 2026 are mixed.

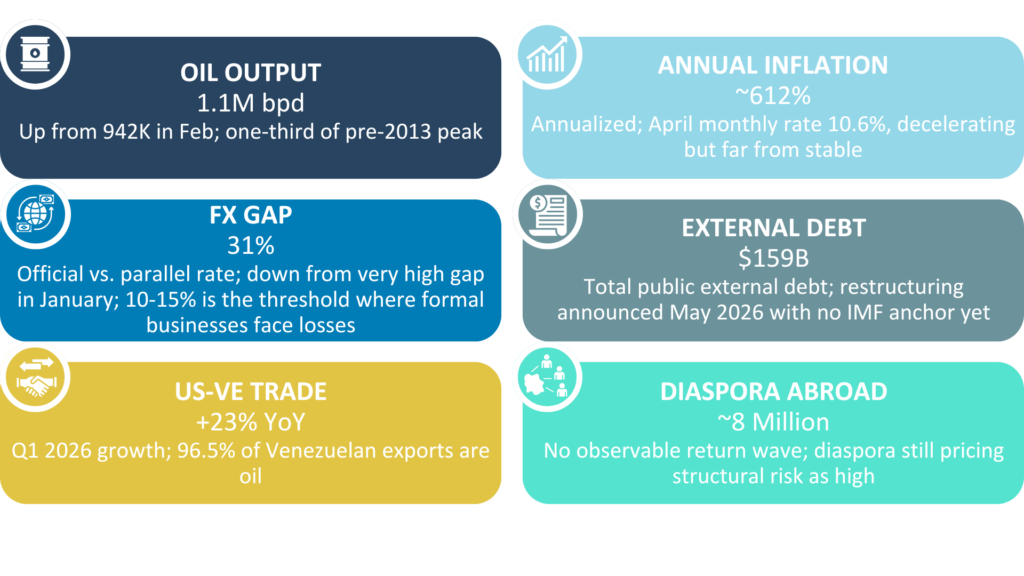

On oil, PDVSA reported an average of 1.1 million barrels per day in March 2026, up from 942,000 in February.2 That is an improvement, driven in part by the easing of U.S. sanctions. But the figure is still roughly one-third of Venezuela’s pre-2013 peak of around 3 million barrels per day. A credible near-term path might add another 500-700 thousand barrels over the next two to three years, but higher output does not automatically translate into more cash for the government, given the complex web of royalties, liabilities, and legacy arbitration claims sitting between the wellhead and the treasury.

On inflation, the central bank reported monthly inflation of 10.6% in April 2026, down from 13.1% in March.3 The annualized rate, however, still stands at over 600%, incompatible with a stabilized monetary system. The government is still financing its deficits partly by printing money, and those on fixed wages pay the price as purchasing power erodes before prices adjust.

On the exchange rate, the gap between the official bolivar rate and the dollar rate on the street has narrowed to about 31%. The relevant threshold, however, is 10-15%. Once exceeded, formal businesses legally required to invoice at the official rate find themselves buying inputs at street prices, creating a self-reinforcing cycle of dollar shortages, informal dollar-based pricing, and renewed inflation pressure.

On electricity, power consumption hit a nine-year high in early May, triggering emergency measures and rolling blackouts, particularly in the oil-producing Zulia region, where outages of six hours a day are again common.4 A grid that cannot keep the lights on is a hard constraint on the industrial and oil-sector revival that stabilization is supposed to support.

02 / Recovery is not Materializing: Investment and Migration Tell the Same Story

Investment is the clearest test of whether Venezuela’s second step, recovery, is taking hold. So far it is not.

Venezuela passed a partial reform of its hydrocarbons law, capping royalties at 30% and introducing a new integrated tax of up to 15% of gross revenue.5 Private operators can now run projects, though PDVSA must retain majority ownership of all joint ventures. The interim government has projected roughly $1.4 billion of new oil investment for 2026.

Chevron and Shell are reportedly exploring expanded operations – but this is a sign of interest, not commitment. Long-term investment requires legal stability, currency convertibility, and political legitimacy that the current environment does not yet provide.

Why Legitimacy Matters for Investment

Without a credible electoral calendar, the safe return of opposition leader María Corina Machado, and the release of political prisoners, investors will continue to price political risk above what the new tax terms can offset. No hydrocarbons reform can substitute for a counterparty whose legal authority is undisputed; foreign operators and creditors need to know that contracts will hold.

The clearest signal comes not from corporate boardrooms but from households. Around 8 million Venezuelans remain abroad, with no observable wave of return migration. The diaspora is still pricing structural and political risks as too high, and the country faces a real shortage of skilled workers for the oil, services, and infrastructure projects that recovery would require.

Trade with the United States did grow; Q1 2026 bilateral trade reached $3.3 billion, up nearly 23% year-on-year.6 But 96.5% of Venezuelan exports in that figure is oil. Recovery in trade is real but extremely narrow.

03 / Debt Restructuring is Outrunning the Macro Framework

On May 13, 2026, Venezuela announced a comprehensive restructuring of its roughly $219 billion in public debt ($159 billion external, $60 billion domestic) and named Centerview Partners as its financial advisor.7 The government committed to presenting a full economic framework and debt sustainability analysis to international creditors by June 2026. That timeline is ambitious and, in DevTech’s assessment, problematic in two important respects.

Concern 1 No IMF Anchor Behind the Analysis

Venezuela only resumed relations with the IMF in April 2026. A debt sustainability analysis presented in June would precede the kind of Article IV review that gives such analyses credibility. Without independent verification of the macro projections, oil revenue assumptions, and fiscal multipliers, the numbers will face skepticism from creditors and multilaterals. Launching a restructuring before a credible baseline is in place means the markets will be buying a story, not a plan. Current bond prices appear to reflect optimism about the restructuring outcome that is not yet anchored to fiscal reality.8

Concern 2 The Wage Increase Does Not Add Up

Public-sector pay was recently raised to around $240 per month, largely through bonuses. DevTech’s DSA scenario modeling shows that hard-currency wage increases above 10% per year push Venezuela’s debt above its pre-shock path and are incompatible with sustainability.9 The announced increase is materially larger than that threshold. To reconcile it with a viable debt path, something else must give: more inflation, larger haircuts for creditors, or new non-oil revenues that have not yet materialized.

A deeper legitimacy question also remains – any restructuring agreement reached under the current political arrangement may face challenges from future governments, particularly if done with a lack of transparency. Creditors factoring in long-duration sovereign exposure should weigh that risk.

04 / Economic Authorities: New Faces, the Same Technical Capacity Gap

Changes at the BCV and the broader economic team have been driven primarily by U.S. sanctions exposure and proximity to Maduro, rather than by a deliberate strategy to rebuild technocratic depth. The acting BCV president, Luis Pérez, has emphasized data integrity in public communications; VP Calixto Ortega has been named Venezuela’s IMF representative.10

What has not changed is the institutional infrastructure that a stabilization-and-restructuring program requires: an independent BCV research department, a peer-reviewed macro framework underpinning the DSA, and timely publication of credible national accounts, balance of payments, and fiscal accounts. The combination of (i) a debt restructuring on a tight timeline, (ii) a stabilization program still in motion, and (iii) limited technical depth at the agencies that must execute both is the single largest source of program-slippage risk over the next 12 months. An IMF-supported adjustment without a credible technical counterpart will struggle to deliver — and to remain politically supportable.

DEVTECH ASSESSMENT: What Would It Take to Move from Stabilization to Recovery?

Step 1 of the three-step framework is partially working but not consolidated. Oil revenues are increasing as oil output is rising and prices are high (and sales are made without discounts). Inflation is still significantly high, reflecting a loose budget constraint for the government, while the FX gap remains unsustainable for the formal sector and electricity is again binding. Step 2 cannot succeed without: (a) a full IMF program behind the DSA, (b) a credible electoral calendar that re-prices political risk, (c) a hard-currency wage path consistent with debt sustainability, and (d) a restored technocratic core at the BCV and Ministry of Finance. These are not optional enhancements; they are preconditions. The most significant near-term risk is sequencing: debt restructuring is outrunning the macroeconomic framework that is supposed to anchor it. Without that anchor, the process risks producing an agreement that creditors will later challenge, and markets are already pricing outcomes that the fiscal numbers do not support.

Sources & Notes

1 Trump Administration Venezuela policy framework: a sequenced three-step approach, Stabilization, Recovery, Democratization (U.S. policy statements, 2025-2026).

2 Oil & Gas Advancement, “Venezuela Oil Output Hits 1.1 Million Bpd Milestone in March,” 2026.

3 Reuters, “Venezuela’s inflation rate eases to 10.6% in April, cenbank says,” May 4, 2026.

4 Bloomberg via Energy Connects, “Venezuela’s Faulty Power Grid Risks Derailing Economic Comeback,” May 8, 2026.

5 Venezuela Organic Hydrocarbons Law reform. January 30, 2026. https://english.news.cn/20260130/d2053a5a8a324bdca3582d7c05df6900/c.html

6 VenAmCham, “Venezuela-US Trade Exchange, Q1 2026,” May 11, 2026.

7 Bolivarian Republic of Venezuela, “Announces the Initiation of a Comprehensive Public Debt Restructuring Process,” BusinessWire, May 13, 2026.

8 DevTech Systems, “Venezuela: Fiscal Space for Wage Increases Under Favorable Oil Price Scenarios,” internal memorandum, April 14, 2026.

12 Bloomberg Línea, PDVSA bond price movement following restructuring announcement, May 13, 2026.

13 Reuters (op. cit.).