")

The new administration in Bolivia has inherited the burden of deep macroeconomic instability and a new political mandate. It must now confront and reverse decades of economic destruction wrought by interventionist, state-dominated socialist policies that hollowed out Bolivia’s productive base, distorted prices, and drained reserves — a pattern all too familiar from Venezuela and Cuba. The International Monetary Fund (IMF)’s most recent Article IV consultation underscores this legacy, highlighting acute fiscal and external imbalances, an unsustainable policy mix, and an urgent need to correct the overvalued exchange rate, rebuild reserves, and pursue credible fiscal consolidation. If the new authorities allow the exchange-rate anchor and subsidy-heavy model to persist unaddressed, the eventual adjustment will be sharper, more painful, and politically destabilizing. The situation is urgent and the challenges significant, but with decisive reform, the new government can restore fiscal discipline and begin rebuilding the economic foundations eroded over years of mismanagement.

Most Pressing Macroeconomic Challenges: Lack of Fiscal Sustainability and Collapsing Exchange Rate Regime

The macroeconomic situation is already pressing. Economic growth has slowed markedly, from 3.1% in 2023 to 1.3 % in 2024, and the IMF expects it to decline further to 1.1 % in 2025 and 0.9 % in 2026. Meanwhile, the inflation rate (end of period) has increased from 2.1 % in 2023 to 10 % in 2024, and it is expected to climb to 15.6 % in 2025 and 16.8 % in 2026.

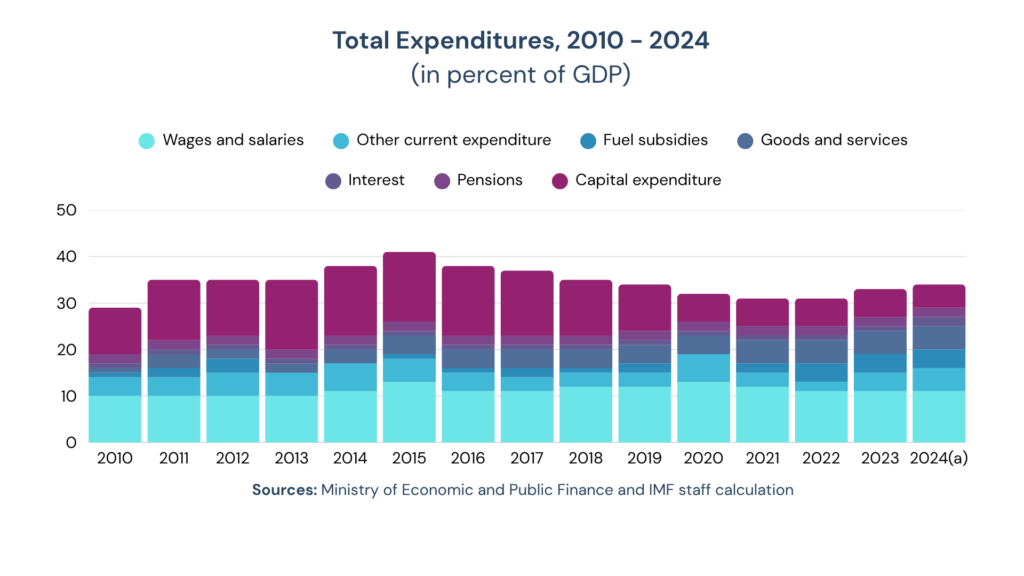

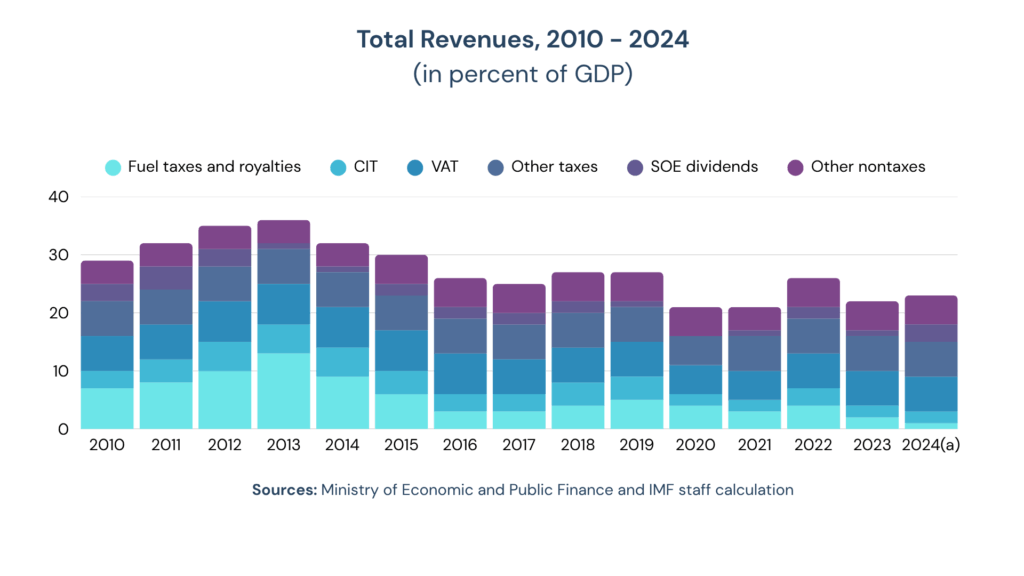

Figure 1. Bolivia expenditures and revenues

Source: IMF Country Report No. 25/116

The two engines of such poor macroeconomic performance are 1) the lack of fiscal sustainability and 2) a collapsing exchange rate regime. The fiscal deficit exceeded 9.8 % of Bolivia’s GDP in 2024 and is projected to remain above 8.5 % in 2025 without corrective measures. Public debt is approaching 95 % of GDP, and interest payments are increasingly concentrated in short-term domestic paper. Tax revenues have fallen from nearly 34 % of GDP in 2013–14 to just 20 percent of GDP in 2024, mostly due to the fall of hydrocarbon taxes. Meanwhile, current spending rose over the past 5 years from about 26 to 32 % of GDP on account of higher wage costs, extensive subsidies, consumption of goods and services, and rising interest payments (see Figure 1).

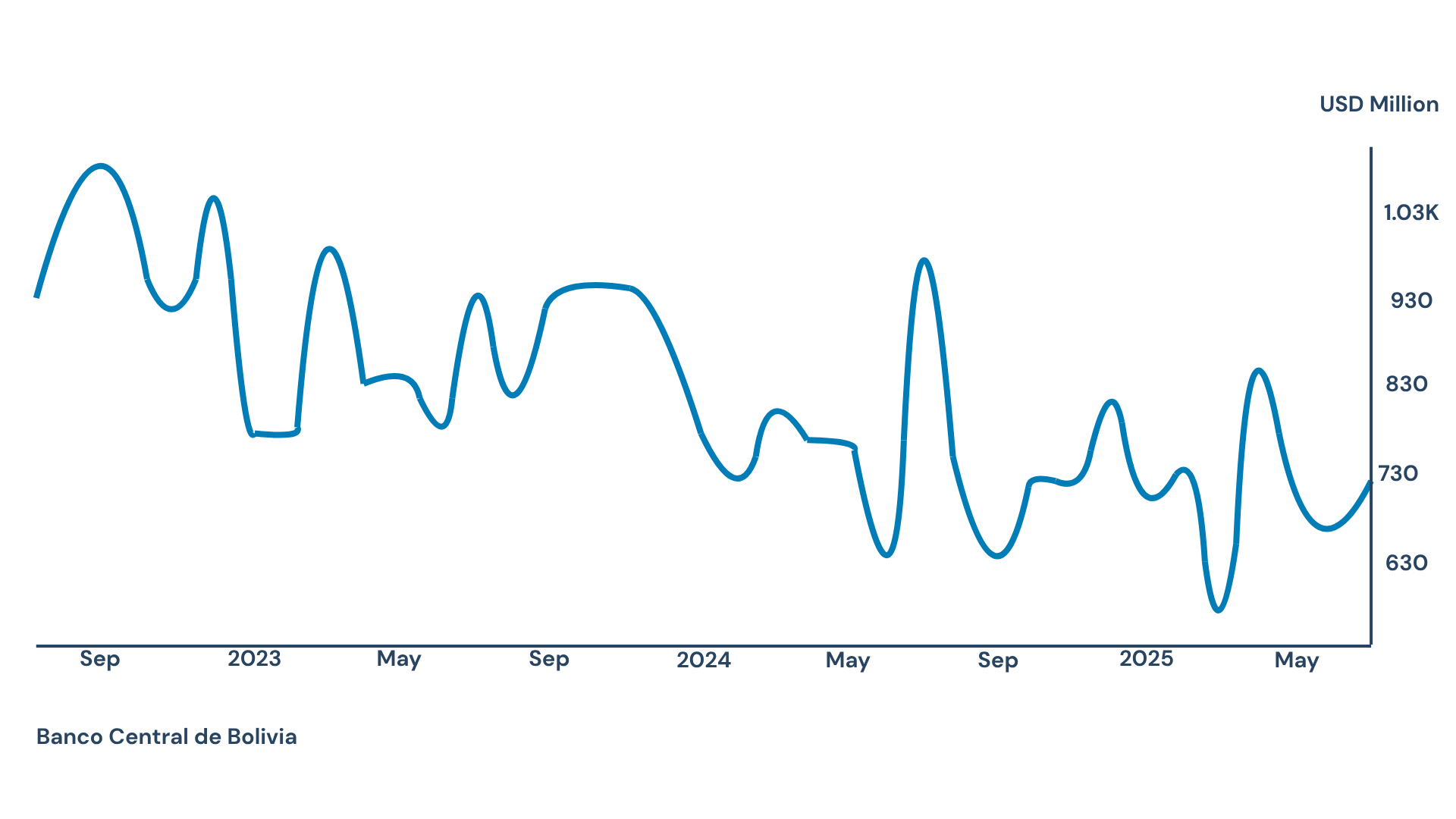

As of September 2025, Bolivia’s gross international reserves had fallen to just under US $2.1 billion, with usable reserves reportedly below US $500 million. Import coverage has dropped to less than one month, and portions of these reserves are tied up in gold and other non-liquid assets. The parallel exchange rate trades 65% above the official rate, and dollar availability through formal channels is increasingly limited to essential imports and selected sectors. This scarcity of foreign currency at the official rate and the increasing depreciation of the parallel rate reduces imports (see Figure 2), disrupts supply chains (which increase production costs), and erodes economic growth.

Figure 2. Bolivia monthly imports

The key to stabilizing Bolivia is tackling two fronts in parallel: the fiscal deficit and the exchange rate regime. The credibility of the entire macroeconomic reset depends on how the authorities manage this interaction and how well they protect vulnerable populations during this adjustment.

Previous administrations accumulated large, unattended macroeconomic imbalances, betting that a favorable shock would make them disappear. For more than a decade, Bolivia’s exchange rate has been pegged with only minimal adjustments — a textbook case of what economists such as Rüdiger Dornbusch and Guillermo Calvo, among others, described in their foundational work on exchange-rate-based stabilization. In their models, anchoring policy on the exchange rate delivers “recession later,” while anchoring on a monetary target delivers “recession now” — the former buys political calm at the cost of a sharper reckoning once reserves run out. Bolivia chose the “recession later” path, sustaining the illusion of stability through cheap imports, subsidies, and dwindling buffers. Those supports have now vanished. What was once a nominal anchor has become a ticking time bomb: the central bank is no longer defending a peg, it is administering a shortage. The IMF’s recent Article IV consultation echoes this concern, warning that if the exchange-rate anchor and subsidy-heavy model persist, the eventual correction will be more abrupt and disruptive. The policy choice ahead is stark — accept a short, controlled “recession now” through credible monetary adjustment, or risk a far deeper crisis when the “recession later” finally arrives.

How to manage the adjustment. Much of the current policy debate is centered on whether the necessary adjustment should be abrupt or gradual. However, this choice is not strictly binary. What matters is designing a credible policy mix that sets the economy on a clear path to reform. This path should correct the main macroeconomic imbalances and deliver tangible benefits to the population within a reasonable timeframe, while managing the potential social impacts of the adjustment.

An immediate move to a floating exchange rate may not be advisable unless backed by decisive international support. At present, Bolivia lacks a nominal anchor strong enough to support a floating exchange rate. However, maintaining the current peg is also untenable given the lack of international reserves and significant fiscal deficits. Alternatives could include a structured transition to a rules-based, pre-announced crawling exchange-rate band. The precise numbers should be determined from detailed calculations, with the most recent data, but several considerations should guide such discussions. The first element to consider is the initial depreciations, which typically depend on the gap between the parallel and official market (e.g., depreciate to half the distance between the official and parallel to around Bs 9.23), as well as the path of reforms that will close the fiscal gap and allow for reserves accumulation. Authorities may decide to adjust the band while the midpoint continues its crawl, subject to review based on three criteria: the pace of reserve accumulation, inflation differentials with the U.S., and domestic inflation expectations.

Such a structure potentiallyprovides the market with a transparent path for adjustment. It would begin depreciation immediately but in a predictable, rules-based way that allows firms, banks, and households to adapt. The transition could stabilize expectations, reduce the parallel premium, and buy time to rebuild reserves. The current administration has the chance to act early, on its own terms, building credibility with the markets and avoiding the negative consequences of disorderly adjustment.

Fiscal Consolidation: Fuel Subsidies and Distributional Trade-Off.

The new administration has inherited a significantly compromised fiscal position, and it must embark on a fiscal consolidation effort to increase taxes and reduce expenditures (particularly the fuel subsidies and the wage bill). In 2024, Bolivia spent roughly 3.7 % of GDP on gasoline and diesel subsidies, more than on public investment. This policy is both fiscally unsustainable and socially regressive, since it benefits higher-income households disproportionately, encourages smuggling, and distorts domestic prices.

The efforts towards fiscal consolidation are larger than the fuel subsidies, but this is a critical aspect of the reforms. For Bolivia, any policy plan must be a credible, multi-year fiscal consolidation. This requires a phase out of fuel subsidies (at least a significant portion of them), a lower wage bill, and a rationalization of capital spending. Delaying these reforms would leave the new government defending an untenable system. Drawing on DevTech’s vast experience in this topic, particularly in hydrocarbon-dependent economies, we understand that while there is no painless path forward, there is a credible one: a controlled, transparent transition that aligns fiscal and exchange-rate policy could restore confidence and set the stage for a more stable recovery. The new administration faces a challenging but achievable path forward, and it can count on DevTech’s expertise to support this delicate process of adjustment.