")

The U.S. faces a stark vulnerability: an overwhelming reliance on imported critical minerals, particularly from China, which controls nearly 60% of global rare earth mining and over 90% of rare earth processing capacity. Of the 12 “strategic defense critical minerals” identified by Silverado Policy Accelerator as posing the greatest risk to U.S. national security,1 China is the top producer of all but one (arsenic trioxide). Additionally, resource-rich nations like Australia, Chile, and the Democratic Republic of Congo produce much of the world’s “battery metals” like lithium, cobalt, graphite, manganese, copper, and nickel, but these raw materials are sent to China for processing, creating a supply chain bottleneck. This monopsonistic arrangement has allowed China to consolidate its power over global supply chains, a strategic advantage that is intrinsically aligned with its broader national security and geopolitical ambitions.

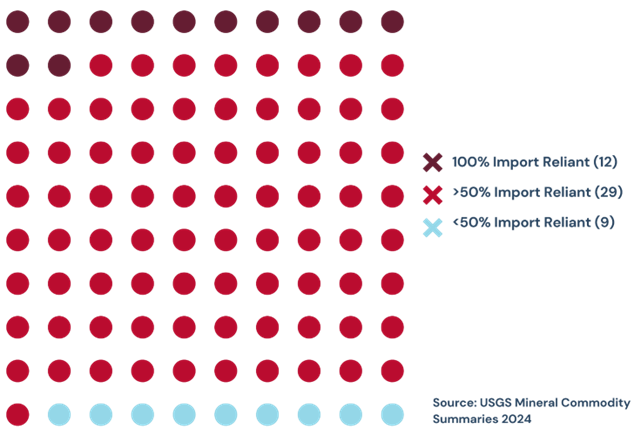

Figure 1. Of the 50 minerals deemed critical by the U.S. Geological Survey, which are the U.S. reliant on?

Out of the 50 minerals deemed critical by the U.S. Geological Survey, the U.S. is 100% import reliant for 12 and over 50 percent import reliant for 29 additional minerals.

Although recent rollbacks in U.S. electric vehicle mandates may slightly temper demand for traditional market-driving minerals like lithium, cobalt, and copper, the overall demand for critical minerals remains robust. Simultaneously, more niche minerals with limited market presence but immense importance to advanced technologies—such as gallium, germanium, and antimony—are subject to escalating supply pressures. Recent export bans by China have highlighted the U.S.’s acute dependence on foreign supply of these materials: 100% import-reliant for gallium, 50% for germanium, and 83% for antimony. With over half of U.S. imports for these minerals sourced directly from China—and even when importing from partner nations like Belgium, Germany, or Japan, there is often upstream exposure to China—supply chains remain vulnerable to strategic manipulation that could erode U.S. hegemony and military power.

Addressing this challenge requires a nuanced approach, as each critical mineral has a unique value and supply chain. Some are byproducts of other industrial processes, others are routinely considered waste, or “tailings,” in commercially viable operations (e.g., antimony alongside gold and tantalum/niobium with tin), and many traverse multiple countries from extraction to end use. Additionally, these materials often lack market prices due to their small quantities and China’s ability to manipulate supply and demand dynamics through non-market practices and its dominance over mid-stream processing.

Critical minerals, therefore, must not be viewed as a monolithic category but as a diverse group of resources with distinct supply chain vulnerabilities. The urgency to develop comprehensive strategies for securing each of these resources cannot be overstated. Overcoming this decades-long deficit will require targeted efforts to ensure supply chain resilience, reduce dependency on foreign adversaries, and balance domestic production with strategic global partnerships.

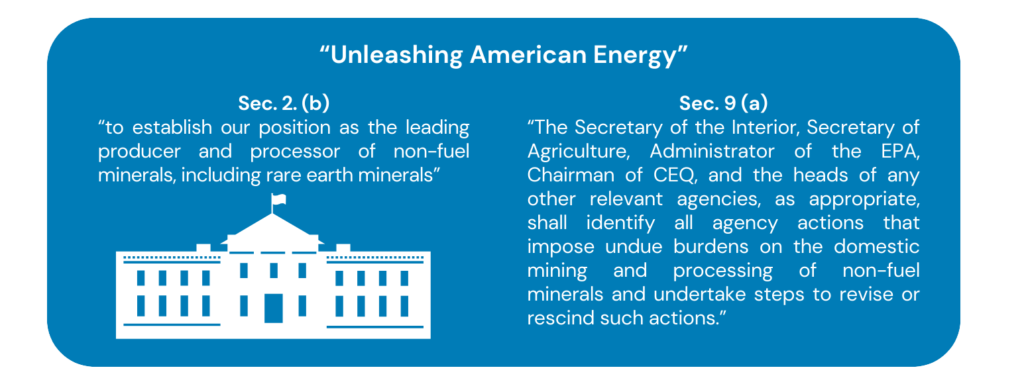

Figure 2. Recent Executive Orders on Critical Minerals

Recognizing this strategic vulnerability, President Donald Trump’s “Unleashing American Energy” and “Declaring a National Energy Emergency” executive orders prioritize the development of domestic critical mineral supply chains. These orders elevate the priority of energy independence, reducing reliance on malign foreign states. Under “Restoring America’s Mineral Dominance,” cabinet officials have been granted such responsibilities as updating critical mineral classifications, accelerating geological mapping, maintaining the National Defense Stockpile, and assessing security implications. Meanwhile “Unleashing American Energy” prioritizes expediting domestic resource development by streamlining the permitting process and incentivizing private sector investment in domestic mining and refining capacity.

These actions signal a strong commitment to reshaping the U.S. critical mineral landscape by instructing agencies to weed out impediments to building our domestic mineral base. However, targeting domestic capacity alone is insufficient for meeting surging demand with resilient supply.

Challenges to Domestic Mining

While these executive orders emphasize boosting domestic capacity, significant challenges hinder the U.S.’s ability to mine and process all its own critical minerals. More specific action items must be identified to minimize mineral dependence and its consequences.

Developing a mine in the U.S. takes an average of 29 years, the second-longest in the world, from first discovery to first production. This is largely due to complex permitting and environmental review processes. While mining companies expect the new administration’s emphasis on resource extraction will expedite these timetables, mining is an inherently disruptive industry. Mining projects such as Nevada’s Thacker Pass face opposition from local communities due to concerns about the strain on local resources, particularly the enormous water requirements, which can lead to shortages or contamination.

Additionally, high operational costs, volatile mineral prices, and limited refining infrastructure can make domestic mining projects financially challenging. This is why strategies informed by comprehensive reviews of domestic resources are essential, along with a thorough review of the entire supply chain. To help ameliorate these inefficiencies, DevTech partner the Critical Minerals Forum (CMF) brings together private sector stakeholders and premier data firms to understand underlying structural prices and supply-demand dynamics. Since there are weak incentives for private sector entities to invest in critical mineral projects given the long lead times and complex risks, the U.S. Government must identify these vulnerabilities and collaborate with the private sector to develop comprehensive strategies and financing arrangements that ensure a secure and resilient supply of minerals. This is especially the case for minerals important to national security but currently perceived as “uneconomical” due to low prices offered by the Chinese market and commercial insignificance by miners looking to turn profits.

The U.S. needs to identify “easy wins” to start diversifying its mineral supply chains domestically. As the executive orders note, many of these resources are already available within the U.S.; we simply need to take stock of material pipelines where critical minerals are currently overlooked. There are existing “legacy” brownfield (abandoned or idled sites that were previously used and still contain valuable resources) mine sites around the U.S. and Canada that require minimal upstart. These could be moved forward through the introduction of financial capital or the expedition of regulatory processes. Additionally, expanding domestic mineral recycling—both from tailings and end-use products—can provide a valuable complementary supply source while reducing the environmental impacts of new mining operations.

While developing domestic mining infrastructure—a process that takes decades—the U.S. can leverage its world-leading energy infrastructure to build its own processing capacity, which is where the competition with China is most dire. Regardless of whether large-scale domestic mining is economically viable or logistically feasible in the U.S., critical raw materials mined around the world are overwhelmingly sent to China for refinement. Even with significant mineral deposits, the U.S. lacks sufficient facilities to process and refine many raw materials into useable forms. Developing such processing and refining facilities represents a tremendous opportunity for the U.S. to solve its critical mineral problem. As China has understood for decades, the value of mining is not in the mine but in the processing of minerals; control over processing equates to control over the market.

Role of Global Partnerships

In addition to prioritizing onshore domestic production—as outlined by the executive orders—and developing processing capacity, to further erode China’s edge in the critical minerals sector, the U.S. must look beyond its borders; this will be essential to derisking supply chains.

Strong partnerships with developing nations can help counterbalance China’s Belt and Road Initiative (BRI), which has consolidated its influence over the global south, particularly global resource-rich countries, by leveraging state-backed financing to secure long-term control over strategic mineral deposits. Rather than relying on traditional supply or offtake agreements—where companies secure future access to mined materials through pre-arranged contracts—China has prioritized direct ownership stakes in high-value mines and issues consistent, serial financing to Chinese companies. According to a new AidData report, only four percent of China’s official sector lending commitments for all BRI projects are guaranteed by a Chinese entity, while 25 percent of lending for transition minerals projects (cobalt copper, lithium, nickel, and rare earth elements) is backed by a Chinese guarantor, suggesting Chinese firms have higher vested interest in the critical mineral sector than in other industrial sectors.

Targeted development assistance in mineral-rich countries would be a significant way of diversifying U.S. supply chains while countering China’s malign and omnipresent control over supply chains from mine to end-use. The U.S. cannot place tariffs on minerals for which it has no feasible capacity to otherwise supply; the country needs to build its stockpile by freeing up funding to support otherwise “uneconomical” projects. Where it is completely unfeasible to develop domestic supply chains for specific minerals, the U.S. could engage with such mining leaders as Canada and Australia. Collaborations could include the transfer of advanced mining and processing technologies, helping resource-rich countries unlock their potential while creating reliable U.S. supply chains. Without coordinated action by market-oriented nations, alongside industry and other stakeholders, these vulnerabilities to Chinese non-market policies and practices are likely to persist.

Another strategic avenue for sourcing critical minerals is Ukraine, whose vast reserves have gained political momentum as a focal point for Western efforts to counterbalance Russian influence and secure diversified supply chains. The Breadbasket of Europe’s extensive critical mineral reserves present a strategic opportunity for the U.S. to secure vital resources while ensuring tangible returns on its support for Ukraine in its struggle against Russian aggression. Resource-rich Central Asian nations like Tajikistan, Kazakhstan, and Uzbekistan have also gained prominence in U.S. geopolitical discussions. These politically popular destinations offer the dual benefit of offsetting Russian and Chinese influence through economic partnerships while serving as an overlooked source of critical raw materials for the U.S.

The U.S. Government’s Development Finance Corporation (DFC), which leverages equity investments, debt financing, risk insurance, and technical assistance, has been identified by the new administration as a key channel that could tailor U.S. foreign assistance in a more strategic manner. The DFC has already begun financing U.S. minerals security, though only about one percent of active projects are in the mining/quarry sector. For example, the Lobito Corridor has been a pivotal investment, revitalizing a 1,300 kilometer rail line running through Zambia and the DRC into the Lobito port in Angola. This project aims to expand and safeguard critical mineral supply chains by enhancing U.S.-led regional connectivity and reducing reliance on Chinese infrastructure.

The DFC should also consider increasing investment in mineral traceability. Manufacturers are willing to pay a premium for a reliable and traceable supply of critical minerals. Traceability is crucial because many resource-rich, developing countries lack strong legal systems, creating opportunities for smuggling and illicit trade. China leverages this smuggling to increase their processing feedstock, while U.S. companies are hampered by “non-conflict mineral” regulations (e.g., 3TG provisions in the Dodd Frank Act). This approach is counterproductive, forcing the issue down the supply chain, and enabling China to dominate the refinement of key minerals without competing U.S. investment. For example, tantalum, a vital mineral in alloys and advanced processors, is subject to ethical concerns about its sourcing. Better traceability would allow the DFC to target low-capital investments for processing capacity in Africa and similar regions. However, the DFC’s current focus on low- and middle-income countries could restrict the U.S.’s investment options for mineral security.

Conclusion

China’s dominance in critical mineral supply chains poses a significant threat to U.S. economic, technological, and national security. Without strategic action, the U.S. risks falling behind in this crucial competition, which will determine future technological advancements, defense capabilities, and global influence.

Meeting this challenge requires a multipronged approach. Domestically, the Trump administration has signaled support for streamlining permitting processes to accelerate domestic mining. In the meantime, however, the U.S. must also take immediate action by:

- Supporting existing brownfield projects,

- Mapping strategies for recovering critical minerals from existing, commercially viable projects, and

- Leveraging world-class energy infrastructure for building out domestic processing capacity.

At the same time, the U.S. cannot afford to ignore the importance of partnerships. Collaborating with resource-rich countries presents an opportunity to diversify supply chains, strengthen economic alliances, and curtail Chinese influence. Strategic intervention through entities like the DFC exemplifies how the U.S. can align foreign assistance with mineral security, easing supply bottlenecks while fostering global stability and innovation.

As a technology-centered firm with an international focus, DevTech Systems looks forward to supporting the U.S. Government in driving these changes, securing the country’s ability to sustainably power semiconductors, defense systems, and AI-driven solutions.