Background

On October 7, 2021, the Government of Indonesia (GOI) passed Law Number 7 Year 2021 on the Harmonization of Tax Regulations (UU HPP). The law revised several existing tax laws and introduced a new carbon tax. This is the first time Indonesia has imposed any taxation on carbon emissions as has been done by 26 other countries to date. This initiative is part of Indonesia’s effort to meet its commitment to reduce carbon dioxide (CO2) emissions by 29 percent on its own or 41 percent with international support by 2030.

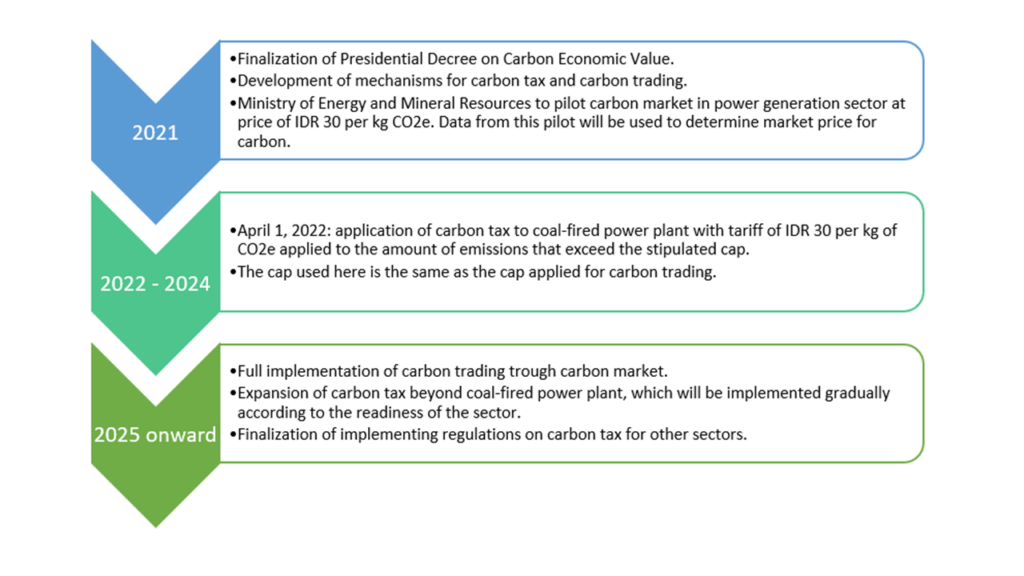

The carbon tax follows a cap and tax scheme, which imposes a tax for carbon emissions beyond a stipulated cap. The GOI is set to pilot the tax in the coal-fired power generation sector beginning in April 2022. In its ambitious aspiration to reduce CO2 emissions, the GOI plans to establish both a carbon trading market system and to expand the carbon tax to other sectors beyond coal-fired power generation in 2025.

Carbon tax as stated in the Law 7/2021 on the Harmonization of Tax Regulations

Purpose: to reduce greenhouse gas emissions in a structured, systematic, significant, and sustainable manner, including both emissions from production processes and individuals’ consumption; to trigger changes in behavior and preferences towards fossil fuels and encourage substitution to renewable energies; and to increase government revenue.

Tax object: Individual or entity that purchases carbon-containing goods and/or engages in activities that produce carbon emissions.

Tax rate:

- By Law, the carbon tax rate is set to be higher than or at market price, with a minimum rate of Indonesian Rupiah (IDR) 30 (US$ 0.002) per kilogram of CO2 equivalent (CO2e), or US$ 2.13 per ton of CO2e emission above the stipulated cap (cap and tax). CO2e is a representation of greenhouse gas emissions that includes CO2, nitrous oxide (N2O) and, methane (CH4) compounds.

- As part of the first stage of implementation starting in April, 2022, the GOI will impose a carbon tax of IDR 30 per kg of CO2e to the coal-fired power generation sector. This rate is among the lowest carbon tax rates in the world and significantly lower than the World Bank and IMF’s suggested carbon tax rate for developing countries (between US$ 30 – 100 per ton of CO2e).

- To determine the cap, the Ministry of Energy and Mineral Resources will pilot a carbon market in the electricity generation sector at the price of IDR 30 per kg of CO2e.

Use of funds: revenue from the carbon tax can be allocated for climate change mitigation efforts.

Tax credit provision: taxpayers who participate in the carbon emission trade, carbon emission neutrality, and other activities as regulated by the environmental law may receive a carbon tax deduction and/or other treatment regarding their carbon tax liability.

Implementation plan

The implementation of carbon tax follows the Roadmap for Carbon Tax, which was approved by the House of Representatives.(1)

Will the carbon tax achieve its objectives?

The introduction of a new tax at a time when the economy is starting to rebound from the COVID-19 induced economic downturn generated strong responses from the public, especially from the business sector that worried about the effect of the carbon tax on the cost of production. Some have criticized the GOI’s initiative describing it as rushed, particularly as international experience shows that effective carbon taxes and carbon markets take years to establish. Meanwhile, others have taken issue with the apparent conflict between the GOI’s new policy of taxing carbon emissions while maintaining subsidies on fossil fuels.

We reviewed the potential effectiveness of the carbon tax to achieve its objectives from the perspective of the principles of good tax policy.

Fairness: the new carbon tax could affect the affordability of electricity putting the GOI’s goal of ensuring universal energy access by 2030 at risk. The potential increase in electricity prices would adversely affect households from the lowest income groups, many of which are considered energy poor.

The increasing cost of electricity could also affect competitiveness given that energy is an input for all production sectors. As electricity costs account for 80 percent of production costs in some industries, the increasing cost of electricity due to the carbon tax would lead to a price increase for consumers, make products less competitive, and possibly disrupt exports.

The conflict among the GOI’s competing objectives related to the carbon tax is understandable. On the one hand, the carbon tax will reduce emissions and contribute to the climate change agenda. On the other hand, continuing the subsidies of fossil fuels will, at least in the short run, reduce the cost of energy to the public. An alternative approach the GOI could consider that is consistent with the goals of both affordability and lower emissions is stimulating renewable energies, many of which have been proven to be cost-effective.

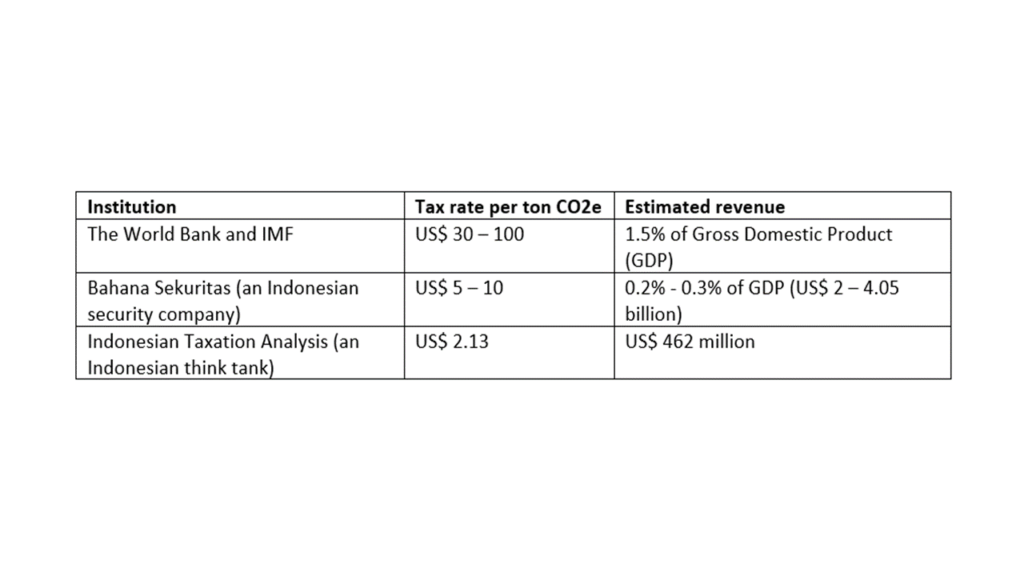

Revenue adequacy: The table included below presents a comparison of potential revenue collection under different tax rate scenarios. The World Bank and IMF recommend a carbon tax rate for developing countries of US$ 30 – 100 per ton CO2e, which should result in a revenue of 1.5% of Gross Domestic Product (GDP). Meanwhile, Bahana Sekuritas (Indonesian security company) estimated a potential revenue of between IDR 29 trillion – 57 trillion (US$ 2.0 billion – 4.05 billion) or 0.2 % – 0.3% of GDP if tax rates are set between US$ 5 – 10 per ton CO2e and imposed to 60% of emission. (2)

The tax rate set by the GOI at IDR 30 per kg CO2e or US$ 2.13 per ton CO2e is one of the lowest carbon tax rates in the world. (3) At this rate, the Indonesian Taxation Analysis (CITA) estimated a potential revenue of IDR 6.5 trillion (US$ 462 million) from the power plant sector alone. The possibility for revenue generation does not seem to be substantial in the early stages of the implementation plan as the rate imposed is very low. This is consistent with the GOI’s statement that revenue generation is not the main purpose of the carbon tax.

On the other hand, the GOI continues to provide subsidies for the use of fossil fuels for power generation. Indonesia argues that the fossil fuel subsidies are meant to preserve electricity supply despite cost fluctuations to protect consumers from electricity disruption and tariff increases. Without proper measures, a carbon tax could inflate fossil fuel subsidies as the GOI may be tempted to increase subsidies to offset the increasing cost of coal for power generation to prevent a significant effect on electricity affordability without adding substantial revenue, therefore putting more pressure on the state budget.

Administrative ease: critics have argued that the GOI’s plan to begin implementing the carbon tax in April 2022 may be rushed, as the GOI only has limited time to prepare the infrastructure, regulations, and enabling environment to support the pilot carbon market and carbon tax itself.

Among other things, the GOI needs to prepare: i) the socialization of taxpayers. The GOI needs to conduct intensive socialization about the purpose, benefit, steps involved for implementation, and evaluation of the carbon tax to prevent its rejection by taxpayers and reduce political and economic risks; ii) the calculation of a market rate for emission taxes, which requires sophisticated calculation techniques that incorporate not only fiscal variables but also climate change measurement variables; iii) clear targets, a list of sectors/sub-sectors to be subjected to tax, standardized measurement methods, and a measurable and transparent monitoring and evaluation framework; and iv) technical guidelines for implementation of the carbon market and carbon tax.

From this perspective, it is unlikely that the administrative requirements will be ready for implementation by April 2022.

Effectiveness in reducing emissions: at the current minimum rate of IDR 30 per kg CO2e, the tax rate is too low to trigger behavioral change. Several businessmen interviewed by The Jakarta Post stated that they would rather pay the carbon tax than invest in new technologies or use renewable alternatives to reduce carbon emissions. Meanwhile, the GOI continues to impose a Domestic Market Obligation (DMO) for domestic coal producers that requires them to set aside 25 percent of their production for power generation at subsidized prices, which guarantees sales of coal to power plants and further demotivates coal producers to reduce production or find greener alternatives for power generation. The continuation of fossil fuel subsidies, including the coal for power generation subsidy, will also reduce the likelihood of behavioral change.

International experience shows that it takes years to establish a carbon market. The GOI’s plan to have a fully operational carbon market by 2025 is therefore ambitious. In the absence of an effective carbon market, emitters would rather pay tax than obtain carbon credit. Accordingly, the GOI’s plan will not lead to a significant reduction in emissions or carbon neutrality.

Conclusion

Indonesia’s initiative to introduce a carbon tax is commendable and shows its determination to fulfill its carbon commitments. However, the current setup of the carbon tax is less likely to motivate changes in behavior and may not contribute to a significant reduction of greenhouse emissions. More effective than stand-alone carbon tax policies as a way for countries to achieve a reduction in carbon emissions are investments in cost-effective renewable sources of energy. A combination of policies in which fiscal revenues from the carbon tax are reinvested into renewable energies could accelerate the desired reduction of carbon emissions. With the right technical assistance and adequate time for its implementation, the carbon tax could be better designed to enhance its effectiveness.

About the authors:

Dr. Renata Simatupang – DevTech Systems Chief of Party for USAID Economic Growth Support Activity (USAID EGSA) Chief of Party

Dr. Jose Pineda – Devtech Systems Senior Advisor and USAID Economic Growth Support Activity (USAID EGSA) Project Director

Teguh Murdjijanto – USAID Economic Growth Support Activity (USAID EGSA) PFM Expert

Footnotes:

- See https://www.esdm.go.id/en/media-center/news-archives/energy-minister-explains-carbon-tax-schemes

- It is advisible to have a carbon tax with a broader scope, covering a wide range of emissions that are subject to the tax because it increases the number of GHG abatement opportunities covered by the policy, as well as the higher tax collection potential of the policy. However, in many cases some sources of emissions are not included as part of the carbon tax mainly due to difficulties in monitoring such emissions. See https://www.energypolicy.columbia.edu/what-you-need-know-about-federal-carbon-tax-unitedstates.

- See https://klikpajak.id/blog/pajak-karbon-dan-tarif-pajak-karbon-indonesia/

References:

- Editorial Board of The Jakarta Post (2021). “Carbon tax, despite paltry rate, has businesses at edge.” The Jakarta Post, October 20, 2021. https://www.thejakartapost.com/paper/2021/10/20/carbon-tax-despite-paltry-rate-hasbusinesses-on-edge.html

- Editorial Board of The Jakarta Post (2021). “New dawn for carbon trading.” The Jakarta Post, October 28, 2021. https://www.thejakartapost.com/academia/2021/10/27/new-dawn-for-carbon-trading.html

- Hindarto, Dicky (2021). “Implementasi pajak karbon di tahun 2022, antara rencana dan tantangan.” Mongabai.co.id, October 11, 2021. https://www.mongabay.co.id/2021/10/11/implementasi-pajak-karbon-di-tahun-2022-antararencana-dan-tantangan/

- Kencana, Maulandy (2021). “Tarik pajak karbon, negara potensi terima Rp. 6.5 triliun dari pembangkit listrik.”Liputan6.com, October 8, 2021. https://www.liputan6.com/bisnis/read/4679291/tarik-pajak-karbon-negarapotensi-terima-rp-65-triliun-dari-pembangkit-listrik

- Klikpajak.id (2021). “Pajak karbon berlaku! Ini tarif carbon tax perusahaan di RUU HPP”. https://klikpajak.id/blog/pajak-karbon-dan-tarif-pajak-karbon-indonesia/

- Kristianus, Arnoldus (2021). “Implementasi perdagangan dan pajak karbon: harus smooth dan tidak timbulkan shock.” Investor.id, October 26, 2021. https://investor.id/bumee/268487/harus-smooth-dan-tidak-timbulkan-shock

- Masterson, Victoria (2021). “Renewables were the world’s cheapest source of energy in 2020, new report shows.” World Economic Forum, July 5, 2021. https://www.weforum.org/agenda/2021/07/renewables-cheapest-energysource/

- Metcalf, Gilbert (2019). “Carbon taxes: what can we learn from international experience?”. Econofact.org, May 3, 2019. https://econofact.org/carbon-taxes-what-can-we-learn-from-international-experience

- Price, Roz (2020). “Lessons learned from carbon pricing in developing country”. Institute of Development Studies Helpdesk Report. April 30, 2020. Lessons_learned_from_carbon_pricing_in_developing_countries.pdf

- Redaksi DDTCNews (2021). “Simak, ini skema pengenaan pajak karbon dalam UU HPP.” DDTCNews, October 13, 2021. https://news.ddtc.co.id/simak-ini-skema-pengenaan-pajak-karbon-dalam-uu-hpp-33577?page_y=0

- Redaksi DDTCNews (2021). “Roadmap pajak karbon di Indonesia 2021 – 2025.” DDTCNews, October 15, 2021. https://news.ddtc.co.id/roadmap-pajak-karbon-di-indonesia-2021-2025-33700?page_y=900

- Thomas, Vincent (2021). “Fossil fuel subsidies will likely render carbon tax useless: CPI.” The Jakarta Post, October 29, 2021. https://www.thejakartapost.com/news/2021/10/29/fossil-fuel-subsidies-will-likely-render-carbon-taxuseless-cpi.html